Paradigm change in real estate

From fixed income surrogate to total return investment: Finding a way out of real estate’s self-inflicted misery

Currently only in English

Everyone who talks to professionals in the real estate industry these days notices it within a minute: our whole bunch is in complete misery mode. We see virtually no new capital raises for real estate funds as investors’ appetite is cold to lukewarm at best. Why? Investment-grade corporate bond funds yield 4 % which is pretty much the same as – or actually higher than – core real estate funds’ cash-on-cash return. Fixed income portfolio devaluations have (technically speaking) made real estate allocations loom large. Everyone is fed up with the term “denominator effect”. This situation raises many questions: Isn’t real estate an asset class to offer (at least partial) inflation protection? With attractive club deal opportunities arising in an adjusted market environment, can’t we achieve above-average total returns that have an accretive and beneficial impact on our investors’ portfolios?

Yes, we can. But the worst is yet to come. We have an idiom in Germany that states: “There is a valley of tears ahead of us”. It means that one must cross a very harsh and challenging environment to climb the next mountain peak. Such a journey is painful, and it will likely lead to serious injuries.

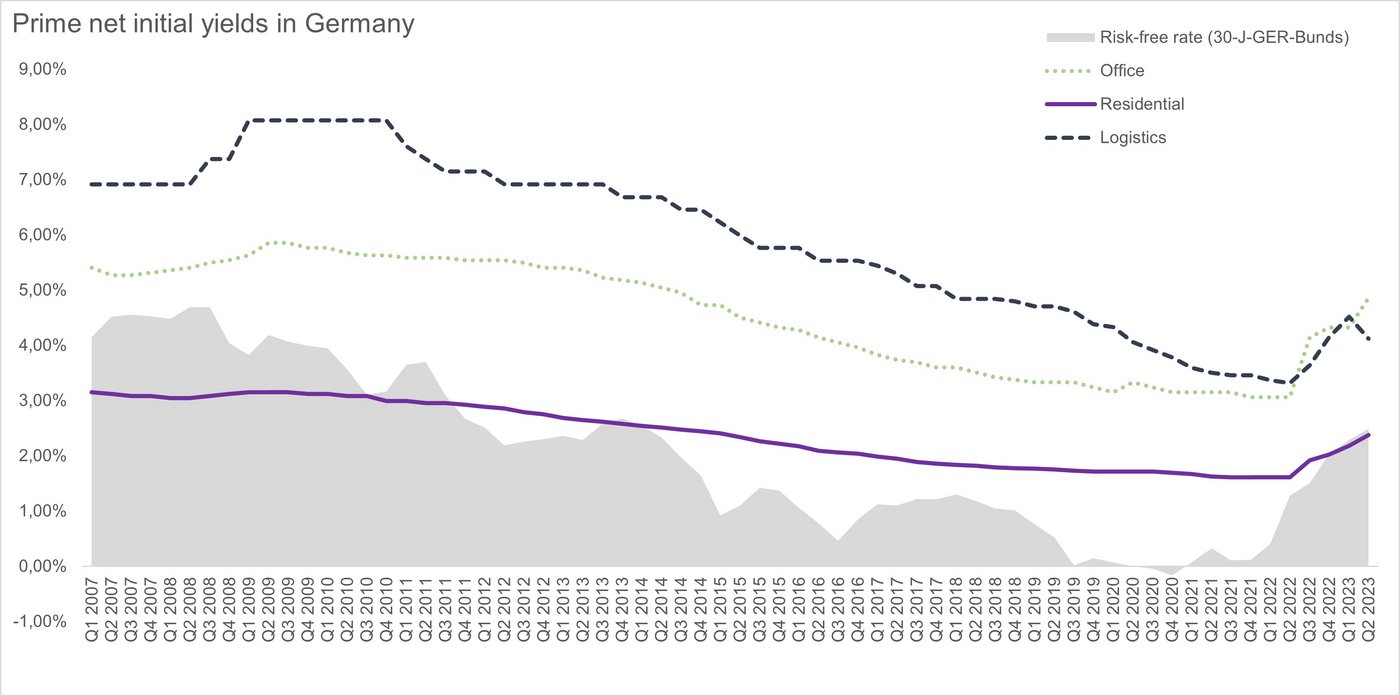

But why? The current misery is clearly self-inflicted. The reason is found in the way real estate was presented as an asset class in the last market cycle, roughly between 2013 and 2021. In an environment shaped by ultra-low and or even negative interest rates, real estate as a fixed-income surrogate became the “new normal”. Does anyone remember the key market slide in all of our pitch decks? It showed the “cap rate spread” – the difference between real estate yields and 10-year government bonds. Due to the abnormally low bond yields, it showed record high spreads despite low real estate cap rates. As a result, initial dividend yields for real estate investments emerged as a crucial selection criterion for many investors.

We have all utilized these charts in our investor presentations, so we are all to blame. Now interest rates are back to where they were early in the last market cycle and investors are seeking fixed income safe havens and the spread has all but disappeared. Basically, the key argument for real estate was flushed away by the central banks moving away from quantitative easing at record pace. Thus, we need to change our narrative substantially for the market dynamics of the next cycle: Growth is the new security.

Growth is the new security – an investment case for the next five years

Looking at (initial) cashflow returns compared to other asset classes is certainly not unreasonable, but only part of the equation. So we have to move away from a “single predictor” to a more complex picture. The investment case is real estate as a total return asset class where the income part of the return plays a critical and usually dominant role. Capital appreciation is derived from long-term income growth and vice versa – capital is destroyed where cashflows become unsustainable. I am convinced that this creates a more comprehensive concept of real estate in a diversified portfolio of financial assets. To make it very clear: Traditionally, real estate represents an operational asset class where the majority of long-term returns are derived from operational performance while the majority of downside risk is derived from investment markets. Long-term value growth, inflation protection, and hence a total return superior to fixed income requires one thing first and foremost: cash flow growth. Rents that grow faster than costs can compensate interest rates rise (typically in an inflationary environment).

Operational real estate and ESG at the forefront

Drilled down this implies a total return focus is not limited to the real estate investment’s (initial) coupon but at long-term value drivers such as rental growth, returns on ESG measures and substantial value creation through vertically integrated services. That means the business model behind a property becomes more important…again. Generating a return by solving the needs of the end-users in a property and the respective underlying businesses and industries is key to achieving tangible benefits and diversification for investors. Therefore, the age of easy money in real estate is over, the low-hanging fruits have been harvested and some of them seem to be quite poisoned. A long lease duration is not a KPI anymore, but income characteristics related to sustainable growth are becoming the key issue. Investment managers need in-depth expertise – a real understanding of the end-users' needs to capture this.

Given these dynamics, investment managers must adapt to the new reality, not only in terms of pricing but also in executing capital expenditures and managing the ongoing sector reallocation wave. Integrated platforms that possess expertise in both development and management are likely to emerge as winners in this paradigm shift. On the other hand, platforms overly exposed to passive buy-and-hold strategies, especially in office markets, will need to align with the new market dynamics and are going to suffer if they can’t or don’t.

We are firm believers in the future of real estate as an asset class. The opportunities arising in this upcoming market cycle can create superior and stable returns for avant-garde investors rethinking the role of real estate in their portfolios. For those that are able to execute this, it will become clear that the normalized interest rate environment offers more opportunity than risk in the mid- to long run. Let’s use these opportunities!

Author: Thomas Kallenbrunnen, Managing Director of GARBE Institutional Capital